Chevron

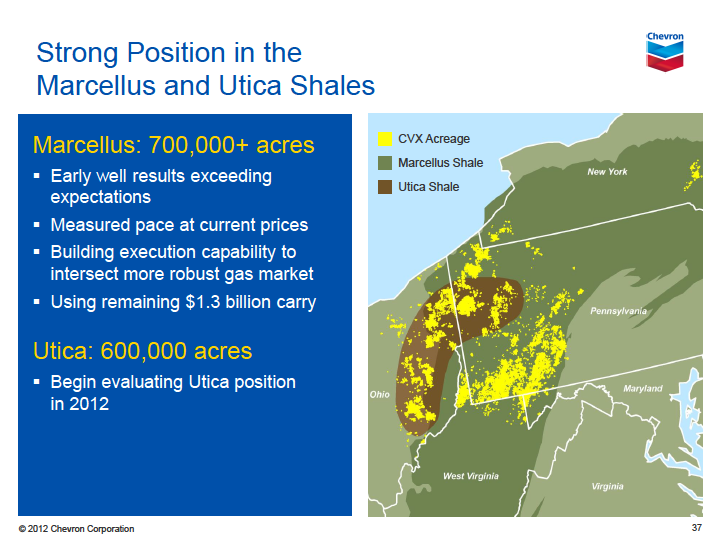

700,000 acres

March 13, 2012 |

EQT

9.0 Bcf Core Defined

March 12, 2012 |

Anadarko

2014 Roadmap

March 13, 2012 |

MarkWest Energy

Play Rankings

March 7, 2012 |

Chevron owns 700,000 acres in the Marcellus, ~180,000 of which are in the wet gas window. CVX made a major move into the Marcellus with its $4.3B buy of Atlas Energy in Nov. 2010, with another $1.6B spent in May 2011 for acreage from Chief Oil & Gas. At current prices, CVX is pursuing the play at a "measured pace". In Q4 2011, CVX had 10 rigs in the play and in early March had ramped down to 6 rigs. Driving CVX today is building internal capabilities to intersect a more robust gas market. |

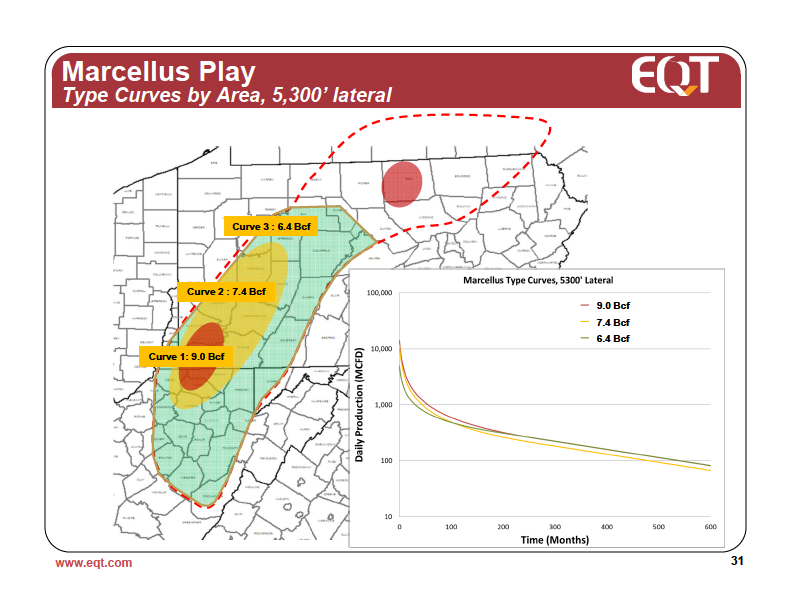

Leading Appalachian E&P company EQT has 530,000 Marcellus acres. Slide above shows the core 9.0 Bcf area along with a defined 6.4 Bcf area. In the core, EQT owns 162,000 acres with 1,330 drilling locations. Using type curve parameters of 7.3 Bcfe EUR and$6.7 MM well costs, EQT presents after-tax returns of 43% at $4.00 gas. At $3.00 returns remain positive. EQT plans to drill ~135 wells in 2012 (up from ~115 in 2011) and recently had 3 rigs running. |

At a recent investor conference, Anadarko gave a series of presentations, including a view of gas price to 2017. In the Marcellus, termed the lowest-cost gas play in the U.S., APC's EUR is 8 Bcf and the company has 5,000+ drill sites on 760K gross (260K net) acres. As the slide above shows, APC is planning on running 13 rigs in 2012 to drill 200+ wells (based on $3.25 gas). APC is sees a 2014 Marcellus drilling ramp up in concert with gas price recovery when its Marcellus program increases 9X. |

Midstream player MarkWest Energy Partners, LP is a leader in the NE U.S shale plays. In the Marcellus (Liberty), MWE is building midstream capability, incl. ethane cracking support, to handle in excess of 1.7 Bcf/d. Ethane cracking will provide Marcellus operators another economic boost. The slide above shows comparative play economics. The wet gas Marcellus area (SW Pennsylvania) ranks #1. Central and NE Pennsylvania rank #4 and #5, respectively.

|