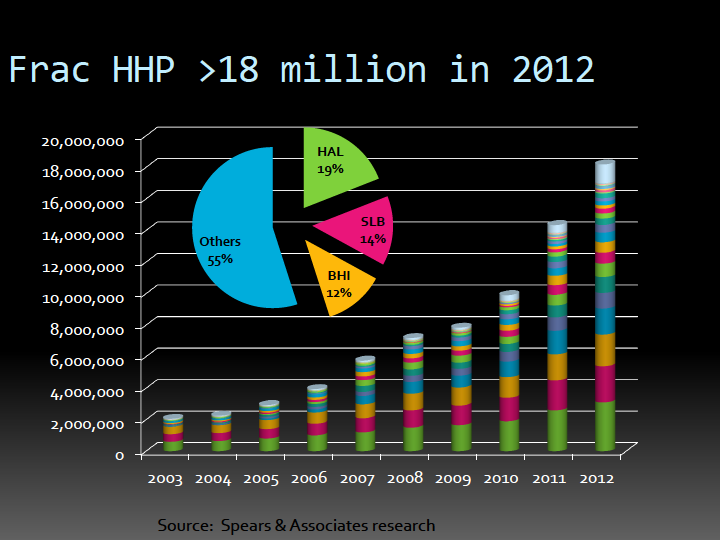

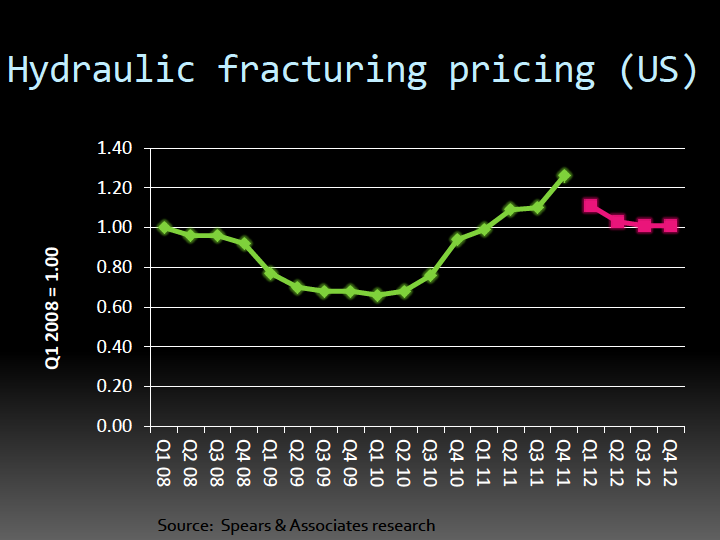

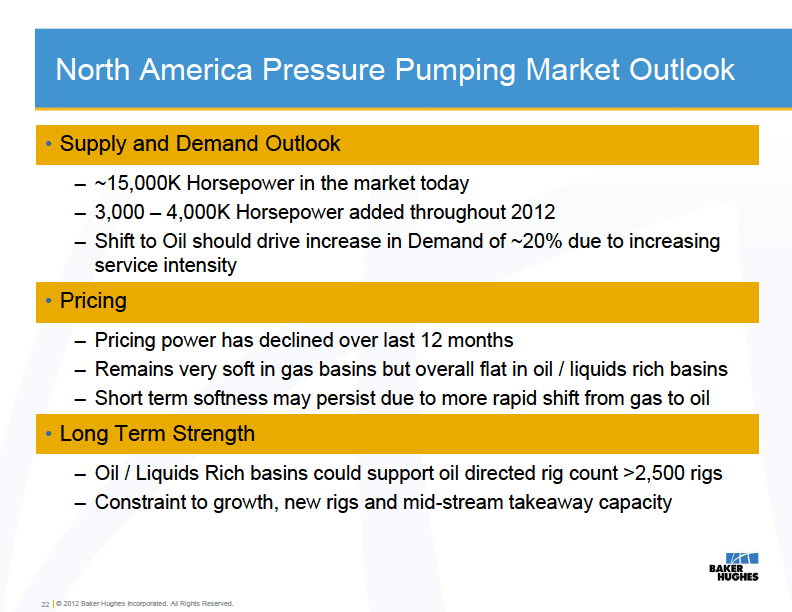

BHI: Pressure Pumping

February 15, 2012

|

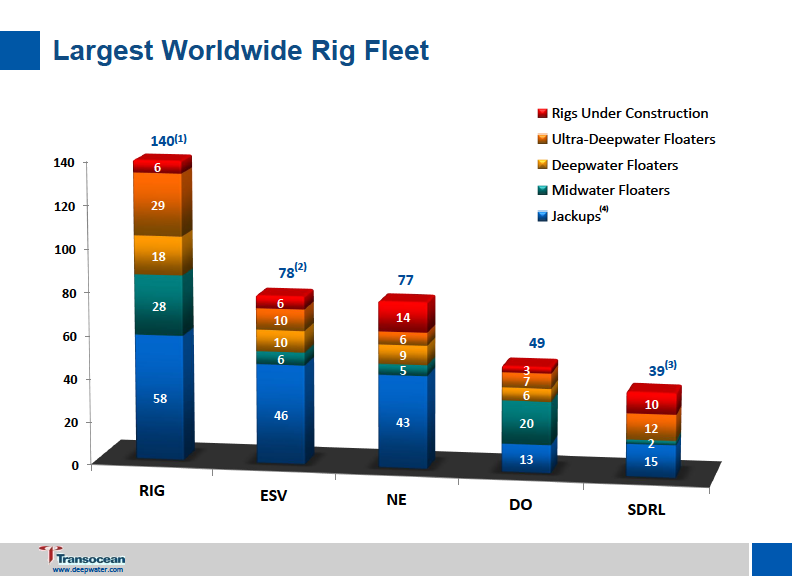

RIG: Strong Visibility

February 07, 2012

|

HAL: Intl. Shales

February 07, 2012 |

WFT: Service Costs

December 6, 2011

|

Baker Hughes also presents North American pressure pumping outlook. BHI expects its pricing power to remain soft in gas basins but overall flat in oil / liquids rich basins (following a decline in pricing power over last 12 months). The short term softness in pricing may persist due to a increasing shift from gas to oil. Longer term, constraining growth in oil basins could be rigs and mid-stream takeaway.

|

Transocean is the world's largest offshore drilling contractor with 140 drilling units (including 6 currently under construction). With strong visibility, RIG currently has $23.5 billion of contract revenue backlog, $8.4 billion which is in 2012. Revenues are diversified with 35% from IOC's, 35% from NOC's and 30% from Independents. RIG's ultra-deepwater fleet is a core strength of the company. |

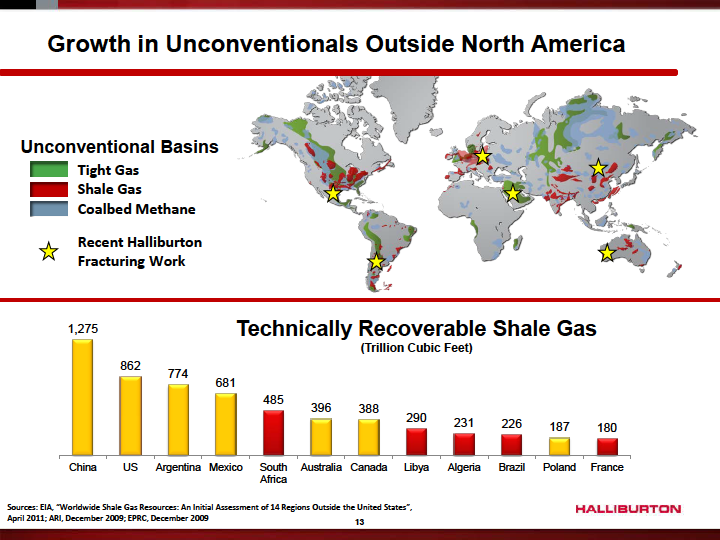

Halliburton expects unconventional activity in international shales, tight gas and CBM projects to be a dominant market driver for the upcoming cycle. The slide above clearly shows China as a huge player with 1,275 Tcf of potential (vs. 862 Tcf in the U.S.). HAL's recent fracturing work internationally includes China, Argentina, Mexico and Poland. HAL's expertise is being exported globally with new teams built locally. |

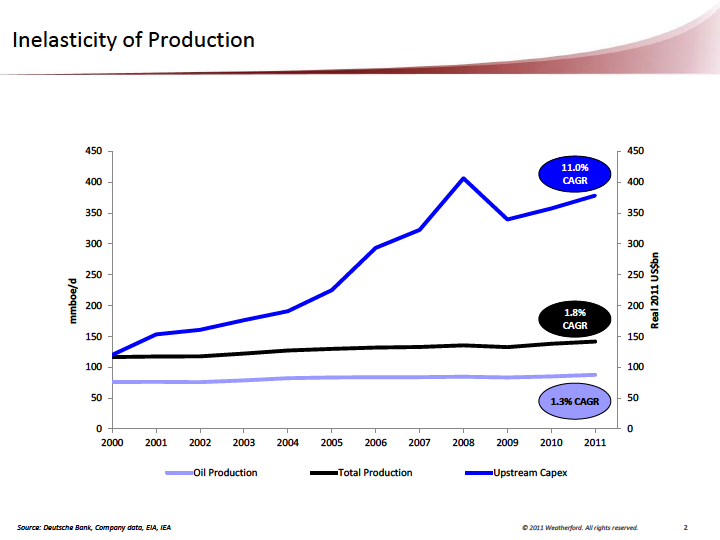

Weatherford's core production business falls under two lines : Artificial lift systems and Production optimization. Currently, there are 350,000 wells on WFT's system, including NOC's and the top 75% of U.S. liquid producers. The slide above shows global production growing at a CAGR of 1.8% since 2000. In the same time frame, upstream spending has increased at a CAGR of 11%. Concluding, inelasticity of production. |