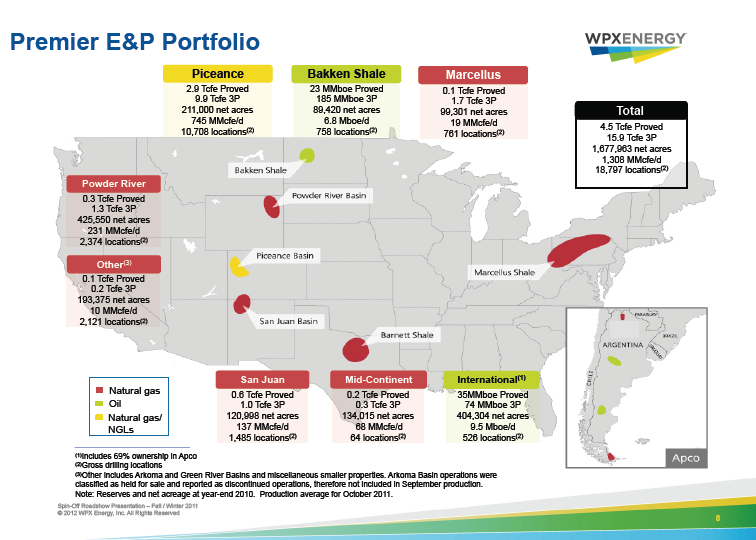

WPX : Portfolio

December 5, 2011 |

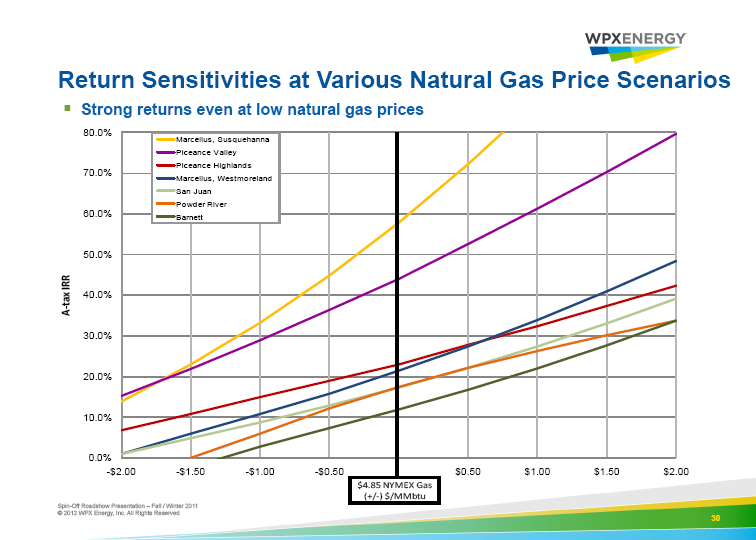

WPX : Gas Sensitivity

December 5, 2011 |

Halcon : New Launch

February 9, 2012 |

Halcon : Portfolio

February 9, 2012 |

WPX Energy is the E&P spin off from Williams Companies. The slide above captures the portfolio : 4.5 Tcfe proved reserves, 15.9 Tcfe 3P reserves, 1.7 MM net acres, 1.3 Bcfe/d of production and nearly 19,000 drilling locations. From 2005 to 2010, WPX's production growth has a CAGR of 13.1%. Based on this relative to E&Ps's that now produce > 1 Bcf/d, WPX ranks #4 behind Southwestern, Chesapeake and Anadarko. |

Given current NYMEX gas prices, the slide above provides another economic benchmark for select gas plays. This one presents after-tax IRR's for 7 of WPX's plays. For this snapshot in time, and for WPX's economics and even at gas prices of $2.85/MMBtu, the Susquehanna Marcellus and Piceance Valley deliver after-tax returns well in excess of 10%. However, the Barnett and Powder River plays break down at prices less than $3.35/MMBtu. |

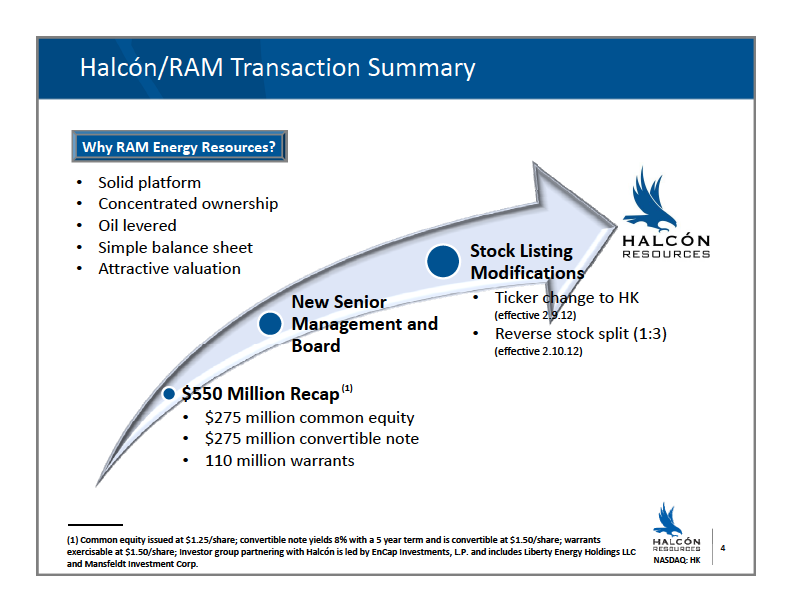

Led by Floyd Wilson (ex Petrohawk leader), an investor group including EnCap, Liberty Holdings and Mansfeldt Investment Corp and a $550 million recap, Ram Energy has become Halcon Resources -- with a NASDAQ Ticker effective 2/9/12 of HK! The gameplan is not surprisingly consistent with Floyd Wilson's prior successes. Follow a proven model, a simple structure, watch costs and create value for shareholders. |

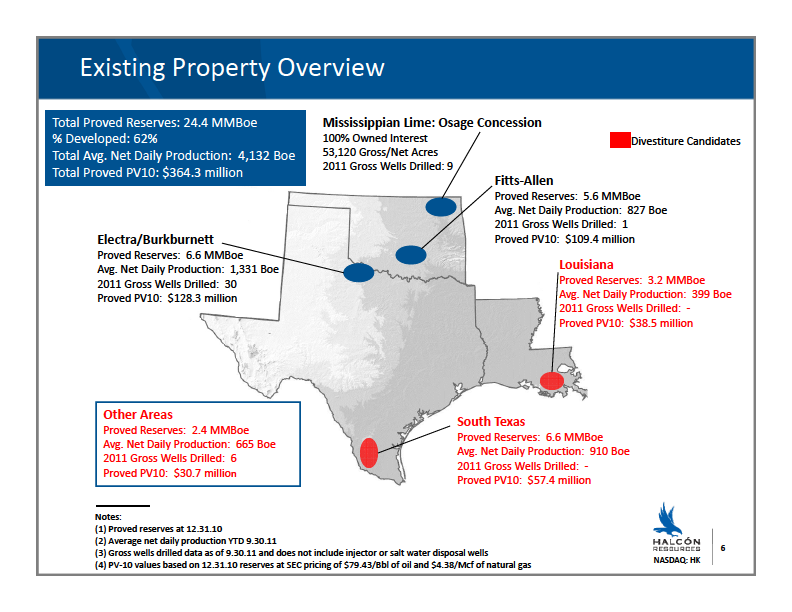

Halcon utilized Ram Energy as its public vehicle route citing, among other things, an attractive valuation, simple balance sheet and leverage to oil. The above shows the existing portfolio. For sale are 50% of the reserves, all of which are > than 70% gas, including south TX and south LA. Staying is Mississippian Lime resource play and conventional waterfloods in the Cisco (TX) and Hunton and McAlester (OK). |