|

| |||||||||||||||||||

| |||||||||||||||||||

| |||||||||||||||||||

| |||||||||||||||||||

Source: PLS M&A Database | |||||||||||||||||||

| |||||||||||||||||||

| |||||||||||||||||||

| |||||||||||||||||||

|

| |||||||||||||||||||

Cooler weather pumps up gasSome think natural gas prices could be in for a rally over the next few days after falling to 11-month lows last week. Prices have suffered recently on decreased demand and on delay of the start of the winter heating season. But meteorologists are now predicting cooler temperatures will start moving in on most of the country, ending the short Indian summer that has brought about unseasonably warm weather on the East Coast. Last week saw natural gas prices settle at $3.47/MMbtu Friday, down 4.5% for the week. It was the fourth consecutive weekly decline in gas prices mostly on weak demand. In New York and Boston this past week temperatures were in the low to mid-80s at a time when temperatures would normally be in the low 60s. The mild temperatures have extended the so-called Fall "shoulder season" for natural gas, which is the period after consumers shut off their air conditioning but before they crank up their heaters. All this mild weather has caused natural gas to build up in storage at a faster pace than normal. The government reported a 97 Bcf injection into working gas storage for the week ended September 30th, which was far above the five-year average injection for this time of year of 74 Bcf. The above-average builds in storage over the last few weeks, combined with a lack of a disruptive hurricane season, has almost made up for the weak supply injection numbers seen during the summer when high temperatures led to an increase in cooling demand. Storage now stands at 3.409 Tcf, which is 78 Bcf or 2.2% lower than where it was last year at this time and 28 Bcf or 0.8% from the five-year average. But the Indian Summer seems to be cooling, which could see storage injections decline. Temperatures over the next two weeks in the Northeast are expected to cool to levels that will produce an above average demand for natural gas, according to Commodity Weather Group. While no major chill is expected, temperatures should fall to levels that will cause East Coasters to shut their windows and dust off their furnaces. The prospect of cooler weather helped natural gas futures reverse course in yesterday's trading session, settling 4% higher from Friday's close to $3.61/MMbtu. Prices are expected to strengthen from their current yearly lows as the heating season kicks into full gear, but analysts expect them to stay relatively weak given the strong storage levels. On the trading side— Traders have started to believe in gas again. Last week, money managers moved to cover their bearish positions in gas by purchasing bullish contracts. This caused the natural gas market to flip from being net bearish to net bullish for the first time in weeks. This is a positive indicator, which usually points to higher prices in the near future. The group is now net bullish by 6,138 contracts as of the week ended last Tuesday. But it is unlikely that prices will surge as production remains very strong in the US. The number of natural gas directed rigs operating in the US rose by 12 last week to 935, according to Baker Hughes. Analysts believe that the rig count should be below 800 to see any measurable decrease in storage levels. View Original Article |

Encana to make decision on Kitimat by 1Q12Encana Inc. officials are in talks with six customers in Asia to take delivery of LNG shipments from the proposed Kitimat terminal. Encana and partners EOG Resources Inc. and Apache Corp. plan to make a final decision on the Kitimat project in 1Q12 once an engineering study is complete, officials said. If the project gets the go-ahead, it could be operational by the end of 2015. About 1.4 Bcf of LNG could be shipped to Asia from the terminal. Coinciding with Encana's plan to ship LNG to Asia is its land position in the Horn River basin in the northeast corner of British Columbia. The company controls 278,000 acres at Horn River, about 14% of the available land, and will produce about 95 MMcf/d from the basin. Encana projects production could reach 5Bcf/d by 2020 if processing capacity is expanded. Encana officials project Asia will need to import 15 Bcf/d of LNG by 2020 to keep up with growth.  View Original Article |

Chesapeake releases long-awaited Utica resultsOne analyst called the rates "phenomenal"Chesapeake Energy disclosed initial horizontal well drilling results in the wet gas and dry gas phases of the Utica Shale play in Eastern Ohio and Western Pennsylvania. The company has drilled 12 horizontal wells in the discovery phase of the Utica and has achieved strong initial production success in the wet gas and dry gas phases of the play from this initial drilling. Chesapeake is early in the process of evaluating the oil phase. Results from the first four of the company's completed horizontal wells in the wet gas and dry gas phases of the play include the Buell 10-11-5 8H (Harrison Co., Ohio), which was drilled to a lateral length of 6,418 feet and achieved a peak rate of 9.5 MMcf/d and 1,425 b/d of oil and liquids, or 3,010 boe/d. Two Carroll Co., Ohio, wells tested at 1,530 boe/d and 1,615 boe/d. The Mangun 22-15-5 8H was drilled to a lateral length of 6,231 feet and achieved a peak rate of 3.1 MMcf/d and 1,015 b/d of liquids. The Neider 10-14-5 3H was drilled to a lateral length of 4,152 feet and achieved a peak rate of 3.8 MMcf/d and 980 b/d of liquids. The Thompson 3H (Beaver Co., Pennsylvania) was drilled to a lateral length of 4,322 feet and achieved a peak rate of 6.4 MMcf/d. The company's other eight drilled horizontal wells are completing or waiting on completion. "The rates were phenomenal," said Michael Bodino, head of energy research for Global Hunter Securities. "With $80 a barrel oil and the rates they are putting up, we think this will be a highly economical play," the analyst was quoted by Bloomberg. Another analyst was more cautious. Results are encouraging, but the Utica Shale is so vast it is early to extrapolate results of a dozen wells to the entire area, Fadel Gheit, an analyst at Oppenheimer & Co. was quoted as saying by the Wall Street Journal. The company has 1.25 million net acres (75% in the liquids-rich and oil window) which Chesapeake says represents 40% of all drillable acreage. Chesapeake plans to bring a JV partner by year end which should provide a valuation marker in comparison to the unsubstantiated $15-20 billion ($14,000/acre at midpoint) valuation cited by management. Currently the company has five operated rigs running, ramping to 10 rigs by year-end 2011, 20 rigs by year-end 2012 and 40 rigs by year-end 2014. "Clearly, infrastructure will be needed (ethane is being minimally recovered) and the company has numerous initiatives ongoing to secure processing and marketing arrangements," Wells Fargo analyst David Tameron said in a note to clients. Chesapeake said the production rates reported assume maximum ethane recovery. The company is processing the wet natural gas stream from the three Ohio wells at a nearby processing facility where ethane is currently being minimally recovered due to temporary market limitations. The company has multiple projects and initiatives underway to process and market future production of NGLs including ethane. The company reported more good news - it set new corporate all-time production records. Gross operated production reached 6.1 Bcfe/d and net production exceeded 3.45 Bcfe/d, including ~95,000 b/d of liquids. By the end of 2012 and 2015 Chesapeake plans to increase its net liquids production by 50% and 150% to over 150,000 b/d and over 250,000 b/d, respectively, while maintaining its net natural gas production at current levels. As recently as in 2009, the company's full-year liquids production averaged only 32,000 b/d.  |

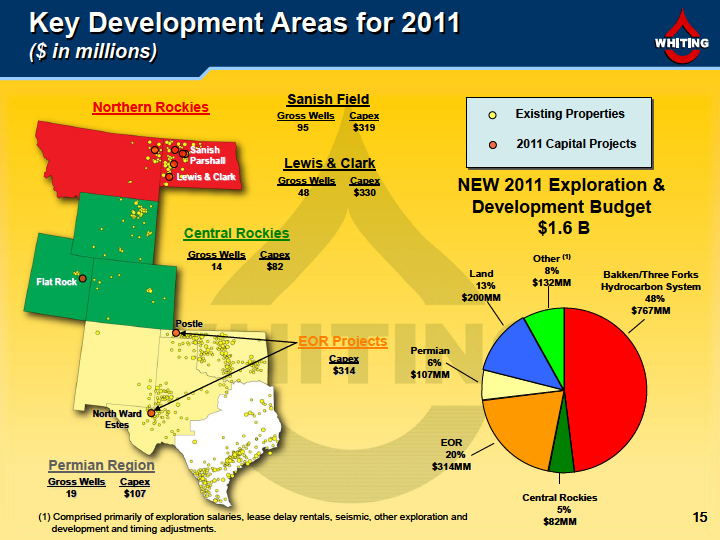

Whiting's Hidden Bench well tests 3,065 boe/dIPs from eleven North Dakota wells average 2,294 boe/dWhiting Petroleum completed 11 notable North Dakota wells, with IP rates ranging from 3,065 to 1,979 boe/d. Speaking at a recent call with analysts, Whiting CEO James Volker said the Lewis & Clark is a "home run," and may be three times as large as Sanish. Volker said the play was one of the best he had seen in his 40 years in the business. Recent results bear out Volker's assessment. In Pronghorn area of the Lewis & Clark prospect, Whiting completed the Smith 34-12TFH in the Sanish Sand formation flowing 2,446 b/d and ~3.0 MMcf/d or 2,939 boe/d. The Smith well, which was drilled on the SE side of the prospect in Stark Co., was fracture stimulated in 30 stages. The Smith 34-12TFH was drilled about a mile NW of the Whiting operated Hecker 21-18TFH, which posted the highest IP rate for any Three Forks well drilled in the Williston Basin at 3,612 boe/d. The Pronghorn area comprises 123,500 gross (114,700 net) acres, which is ~15% larger than the company's Sanish field. Whiting holds a controlling interest in 75 1,280-acre spacing units at Pronghorn. Also at Pronghorn, Whiting completed the Lydia 21-14TFH in the Sanish Sand with an IP rate of 1,960 boe/d. For the year, Whiting participated in 28 wells at Lewis & Clark with an average IP rate of 1,166 boe/d and a 90-day average rate of 356 boe/d. Also at Hidden Bench, Whiting completed the Johnson 31-4H in the Middle Bakken flowing 2,089 b/d and ~2.6 MMcf/d (2,520 boe/d). The well was tested on a 48/64-inch choke with a flowing casing pressure of 600 psi and was fracture stimulated in a total of 30 stages, all using sliding sleeves. The Johnson well is located ~three miles northeast of the Norgard well. For the year, Whiting participated in five Hidden Bench wells with average IPs of 2,669 boe/d and 90-day rates averaging 548 boe/d. View Original Article |